There was an opinion making the rounds today from a chief strategist named Suttmeier that the gold bull market was over because the 50 day moving average has fallen below the 200 day moving average for gold, commonly called a 'death cross.'

Interestingly enough he calls for a trading range, and not a further significant decline in gold, but rather a 5% trading range 'for years.'

During the financial crisis in 2008 gold corrected and consolidated for about one year. In each of the prior three 'death crosses' on the chart the period was about three to six months.

Below is a longer term gold chart that shows that the 50 day moving average has fallen below the 200 day moving average at least four previous times since 2003.

Each time this happened it has marked a consolidation and correction that resulted in gold moving another leg higher and sometimes sharply higher after a prolonged correction. This is climbing the classic 'wall of worry.'

Perhaps it will be different this time. But not based on anything I have seen in technical analysis such as this.

The fundamental drivers of the gold bull market not only remain intact, but seem to be even more compelling based on the fact that central banks have turned net buyers for the first time in over twenty years, as well as recent events in the currency wars regarding the value and security of sovereign debt, which is exactly what the substance of a fiat currency is: sovereign debt of zero duration.

Thanks to my friend Nick Laird of Sharelynx.com who has one of the best and most diverse collections of online charts around.

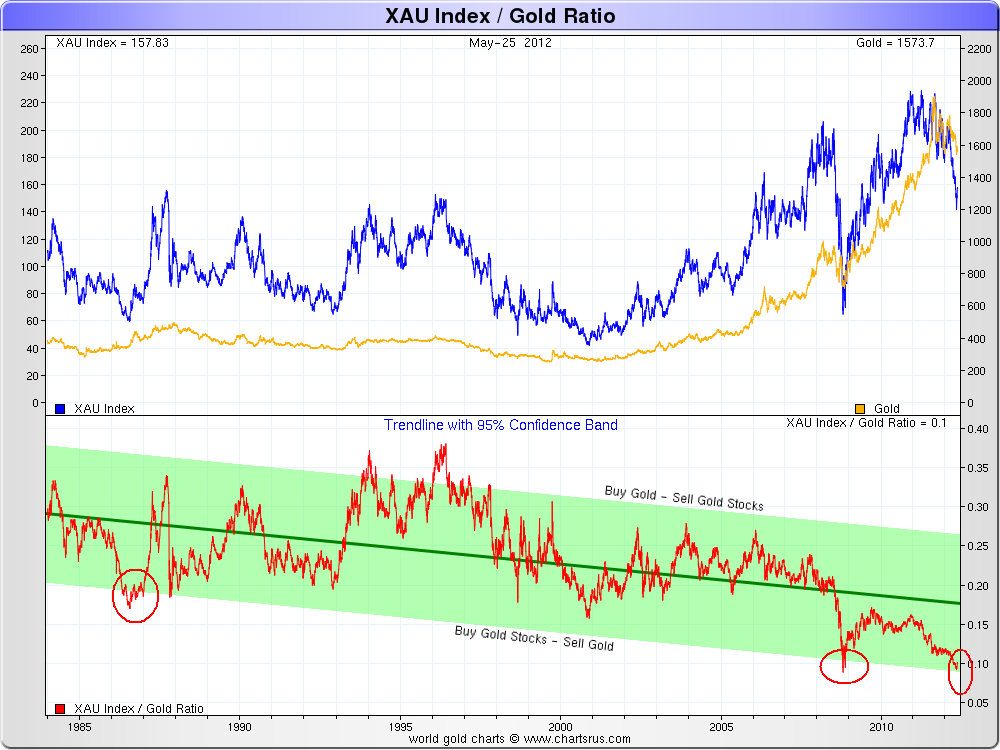

If Europe should collapse and bullion enter a protracted trading range, one might consider buying mining shares of high quality that pay dividends, as they are now quite cheap as shown by the XAU - bullion ratio in the second chart.

As a reminder, in times of crisis I tend to find a safer haven in bullion than in miners, and in gold rather than silver. So let's see what happens in the Greek elections this month, and in the next Fed meeting shortly afterwards.

I tend along with others to think that the central banks must print money to secure the current banking system. That is the raison d'être of a fiat currency system: to be versatilely expansive in repairing the holes made from the inevitable speculative excess caused by crony credit expansion by the Bank for its friends. But in the short term these markets are hardly tied to fundmentals or efficient allocation of capital.

As a reminder we might see a few more antics tied to the June futures contract this week.

May 29

QO - June 2012 COMEX miNY Gold - Last Trade Date

QO - June 2012 COMEX miNY Gold - Settlement Date

GC - May 2012 Gold - Last Trade Date

GC - May 2012 Gold - Settlement Date

May 31

GC - May 2012 Gold - Last Delivery Date

GC - June 2012 Gold - First Notice Date

June 1

GC - June 2012 Gold - First Delivery Date